The Global Gold Game: Why Central Banks and Investors Are Buying Up Bullion

Gold has always been more than just a commodity—it is a barometer for economic uncertainty, inflation fears, and, increasingly, geopolitical maneuvering. In 2024, gold demand surged to a record 4,974 metric tons, primarily driven by central banks and individual investors. While this record-breaking demand might suggest growing confidence in gold as a financial safe haven, a deeper look reveals an unusual trend: a massive physical shift of gold into the United States.

The Surge in Gold Demand

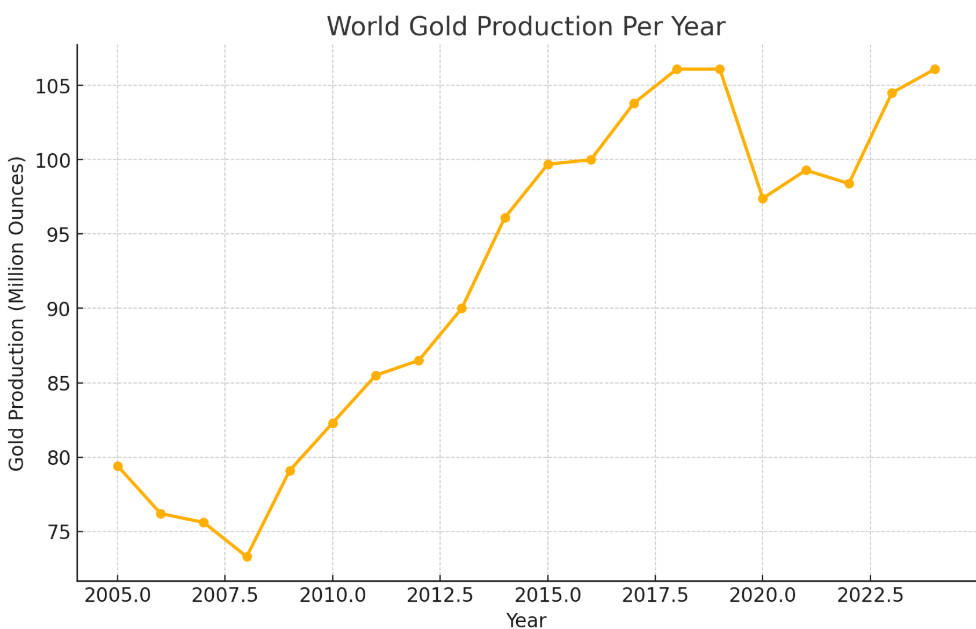

According to the World Gold Council, gold demand in 2024 grew by 1% compared to 2023, with total annual demand reaching an unprecedented level. However, global gold production, at approximately 106.1 million ounces, still falls significantly short of demand, leaving a persistent gap that must be filled from existing reserves and secondary markets.

But what is truly fascinating about this shift in gold markets is not just the increase in demand but where the demand is coming from and where the gold is moving. Historically, gold has been dispersed across various financial centers, but the last several months have seen an extraordinary shift—huge quantities of physical gold have been flowing into U.S. vaults, particularly those of COMEX.

A Political Influence: The Tariff Effect

One of the key drivers behind this trend is tariff uncertainty. The possibility of new trade tariffs, particularly under former President Trump’s rhetoric about imposing 10%, 20%, or even 25% tariffs on imported goods, has led to speculation that gold may also be affected. This has sparked a rush among investors and institutions to bring as much gold as possible into the U.S. before potential tariff changes take effect.

Philip Smith, Group Chief Executive of StoneX, recently pointed out an alarming development: a significant price divergence between New York’s COMEX gold futures contracts and the London over-the-counter (OTC) physical gold market. While December saw the gap widen to nearly $60 per ounce, more recent fluctuations remain between $25 and $30. This discrepancy suggests inefficiencies and uncertainties in the global gold supply chain, reinforcing the urgency for physical gold ownership within U.S. borders.

Smith further revealed that over 2,000 metric tons of gold have been moved into the U.S. in just the past two months, an astonishing figure considering the total annual demand.

The Fort Knox Conspiracy and London’s Alleged Shortage

As with any significant financial movement, speculation and conspiracy theories are running rampant. The surge in gold demand in the U.S. has fueled rumors about Fort Knox, with some questioning whether the U.S. truly possesses the gold reserves it claims. This speculation has been amplified by certain political narratives, though the truth is far less sensational—Fort Knox’s gold reserves undergo regular audits, with the last full physical verification conducted in 2008 and annual paper audits completed each year.

Meanwhile, another popular theory among gold investors is that London is running out of gold, prompting urgent deliveries to the U.S. The reality, however, is more nuanced. While it is true that lease rates for gold in London spiked to over 5% in early 2025, this was a temporary bottleneck rather than a long-term supply crisis. Data from the London Bullion Market Association (LBMA) confirms that while 151 metric tons of gold left London in January alone, total vault stocks still hover around 8,535 metric tons, a level consistent with recent years.

Separating Hype from Reality

Financial markets thrive on narratives, and gold has always been a focal point for extreme theories, from global economic collapse to hyperinflationary panic. However, while it is true that physical gold demand has increased, particularly in the U.S., it does not signal a breakdown of the global financial system.

What this trend does indicate is:

- A continued strong interest in gold as a hedge against economic and political instability.

- The potential for higher gold prices as demand remains strong, particularly if supply constraints persist.

- A shift in investor preference from paper gold (futures contracts, ETFs) to physical gold, suggesting a more cautious approach from institutional buyers.

The Outlook for Gold Prices

Despite the waves of speculation, the fundamental case for gold remains robust. As long as economic uncertainty looms and central banks continue accumulating reserves, gold is unlikely to lose its appeal. Furthermore, the increased mainstream media coverage of gold, partially due to political influences, is likely to keep demand elevated.

For investors, this means gold is no longer just a historical store of value—it is becoming a key asset in global trade and geopolitical strategy. While doom-and-gloom predictions about the financial system collapsing should be taken with skepticism, there is no denying that gold’s role in global finance is evolving rapidly.

As the markets navigate a highly politicized gold landscape, one thing is clear: gold is no longer a “barbarous relic” but a crucial financial instrument in an increasingly uncertain world.

{kind=link}